FATCA regime including:

- Form 8233 or W-4 when receiving compensation for personal services performed within the U.S.

- Form W-8ECI when receiving income effectively connected with the individual’s U.S. trade or business that the individual will report as taxable gross income on a Form 1040NR U.S. income tax return

- Form W-8BEN in all other situations

Foreign entities should complete one of the following forms:

- Form W-8ECI when receiving income that is effectively connected with the entity’s U.S. trade or business, e.g., a U.S. branch, that the entity will report as taxable gross income on a U.S. income tax return, generally on Form 1120-F

- Form W-8EXP when the foreign entity is a governmental entity or not-for-profit organization claiming exemption from Chapter 3 withholding tax under a specific IRC provision

- Form W-8IMY when the foreign entity is either an intermediary not acting for its own account or is a fiscally transparent entity—either for U.S. income tax purposes or for income tax purposes in its resident country, such as a foreign trust or foreign partnership

- The single owner of a foreign disregarded entity for U.S. income tax purposes typically completes the appropriate form under the owner’s name and information rather than the disregarded entity completing a form, except a foreign hybrid entity claiming treaty benefits

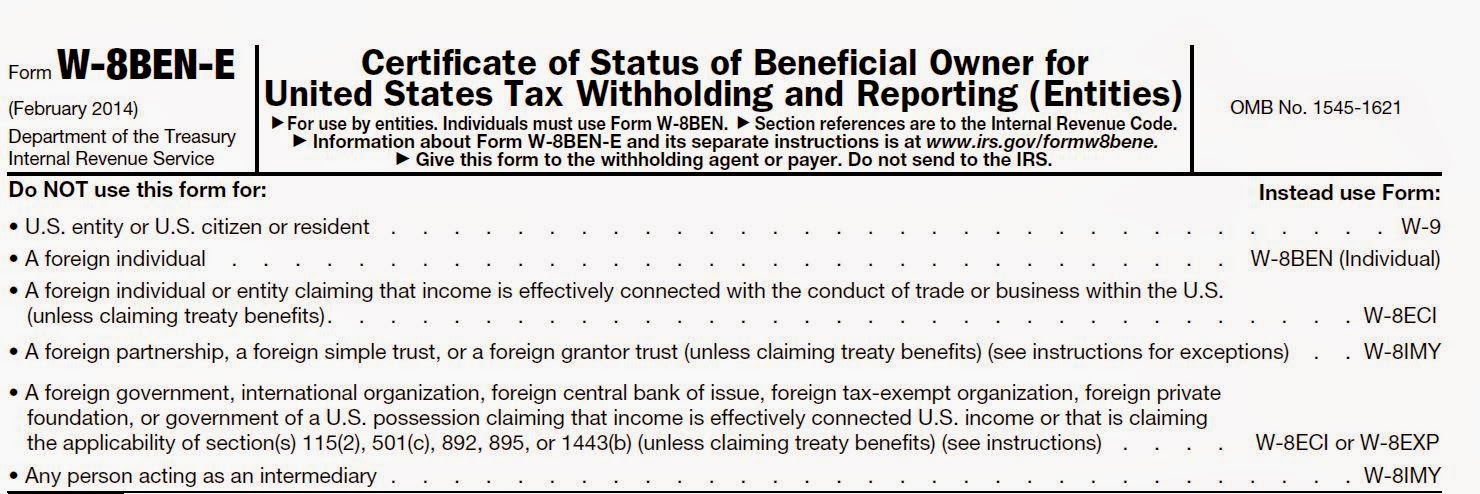

- Form W-8BEN-E in all other situations

The foreign recipient should complete the applicable Chapter 3 sections of the form, including its Chapter 3 status, any claim of tax treaty benefits for Chapter 3 purposes where applicable and any other documentation required for Chapter 3 purposes. Until the IRS publishes instructions for the 2014 versions of Forms W-8BEN-E and W-8IMY, foreign-entity recipients completing those forms may look to the instructions for the 2006 versions of Form-W-8BEN and Form W-8IMY to determine the requirements for Chapter 3 purposes. However, for a Form W-8BEN-E submitted on or after July 1, 2014, a foreign entity now has the option of entering either its U.S. taxpayer identification number or a foreign taxpayer identification number issued by its country of residence in order to make a treaty benefit claim for Chapter 3 purposes.

For nonresident alien individuals and foreign entities completing Form W-8ECI or W-8EXP, the foreign recipient’s Chapter 4 status is either irrelevant, e.g., in the case of a Form W-8ECI, or generally is the same as the recipient’s Chapter 3 status and thus usually doesn’t require any additional analysis. Other foreign entities completing Form W-8BEN-E or W-8IMY should proceed to Step 2.

Step 2: Determine whether the foreign entity is a foreign financial institution (FFI) or a non-financial foreign entity (NFFE)

The FATCA regime primarily distinguishes foreign entity recipients between FFIs and all other foreign entities, called NFFEs. This distinction is not as obvious as it may seem. Certainly the standard business definition of a financial institution is included in the definition of an FFI, but other entities not normally thought of as financial institutions also may fall under the definition of an FFI. The following types of entities generally are treated as FFIs under the FATCA regulations:

- Foreign depository institutions that accept deposits in the ordinary course of banking or similar business

- Foreign custodial institutions that hold, as a substantial portion of their business, financial assets for the benefit of one or more other persons

- Foreign investment managers that primarily invest, administer or manage funds, money or financial assets on behalf of customers

- Foreign collective investment vehicles, such as mutual funds and hedge funds

- Foreign investment entities primarily earning gross income attributable to investing, reinvesting or trading in financial assets having an investment portfolio that is professionally managed by a third-party entity investment manager; many privately held foreign trusts and other privately held foreign investment companies will be swept into this category of FFI

- Specified foreign insurance companies that issue or make payments on life insurance

- Foreign holding companies, treasury centers and captive finance companies that are members of a financial group of affiliated companies

Step 3a: A foreign entity that meets the definition of a foreign financial institution (FFI) should identify whether an Intergovernmental Agreement (IGA) applies, as well as its requirements under the applicable IGA.

In general, for an FFI to qualify for exemption from the 30 percent FATCA U.S. withholding tax on the receipt of a withholdable payment, there must be some form of annual reporting of the FFI’s U.S. accountholder activity to the IRS, similar to Form 1099 reporting required of U.S. financial institutions, as well as withholding of U.S. federal tax from income of U.S. “recalcitrant account holders” who do not provide the necessary Form W-9 documentation to the FFI and other U.S. accountholders that are otherwise subject to backup withholding.

While an FFI may register with the IRS portal on its own to enter into an FFI agreement to become a participating FFI annually reporting U.S. accountholder activity directly to the IRS, the majority of countries and jurisdictions have privacy laws preventing institutions from providing the required accountholder information. To address the privacy issue, the U.S. Treasury Department has been negotiating with other counties to develop IGAs designed to override local law prohibitions. Some IGAs may provide a more favorable definition of an FFI compared to the FATCA regulations. All IGAs are based on two types of model IGAs:

- Under Model 1 IGAs, FFIs report U.S. accountholder activity directly to their local taxing authority rather than registering and reporting directly to the IRS. The local authority then forwards the information to the IRS through automatic exchange of information.

- Model 2 IGAs authorize FFIs to register with the IRS and enter into an FFI agreement to become a participating FFI that reports U.S. accountholder activity directly to the IRS, with slight modifications to take into account local law prohibitions.

Certain FFIs are not required to enter into an FFI agreement if they are deemed compliant.

As part of the registration process on the IRS portal, an FFI applies for a global intermediary identification number (GIIN) that it must disclose on Form W-8BEN-E or W-8IMY for the form to be valid.

For an FFI to determine its specific Chapter 4 status to disclose on Form W-8BEN-E or W-8IMY and determine its reporting and withholding obligations, we highly recommend professional analysis of an applicable IGA by an attorney or certified accountant.

In some cases, an FFI may want to perform a cost-benefit analysis to determine if the burdens of complying with the reporting requirements under an applicable IGA or as a participating FFI outweigh the benefits of avoiding the 30 percent U.S. withholding tax on the receipt of withholdable payments under FATCA. Many FFIs have decided to implement a policy of avoiding investment in assets that produce U.S. source income or refuse to accept U.S. accountholders so that the FFI effectively incurs no penalty for failing to comply with the FATCA reporting requirements as a nonparticipating FFI.

Step 3b: Any other foreign entity that is not an FFI should determine its specific Chapter 4 non-financial foreign entity (NFFE) status and document that NFFE status on Form W-8BEN-E or W-8IMY.

The compliance obligations of NFFEs under FATCA are substantially less involved than for FFIs. In most cases, an NFFE is not required to register with the IRS and merely needs to document its NFFE status on Form W-8BEN-E or W-8IMY to qualify for exemption from the 30 percent FATCA withholding tax.

The following is a list of the different types of NFFEs under FATCA, all of which qualify for exemption from the FATCA withholding tax on the receipt of a withholdable payment, unless otherwise stated:

Publicly traded NFFE – An NFFE that is a publicly traded corporation the stock of which is regularly traded on one or more established securities markets for the calendar year

NFFE affiliate – An NFFE member of the same expanded affiliated group as a publicly traded corporation, including a publicly traded NFFE or a publicly traded U.S. corporation

- An expanded affiliated group is defined under principles of IRC §1504(a) but with a 50 percent control requirement and inclusion of partnerships and foreign corporations

Active NFFE – An NFFE having less than 50 percent of its gross income for the preceding taxable year consisting of passive income and less than 50 percent of the weighted average of its assets that produce or are held for the production of passive income

- Passive income includes most types of investment income, including dividends, interest, rents, royalties, annuities, amounts received under cash value insurance contracts and amounts earned by an insurance company in connection with its reserves

Excepted Territory NFFE – An NFFE that is directly or indirectly wholly owned by one or more bona fide residents of the same U.S. possession in which the NFFE is organized or incorporated, including those organized in Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa and Northern Mariana Islands

Excepted NFFE – There are several categories of excepted NFFEs:

- Holding companies, treasury centers and captive finance companies that are members of a nonfinancial group

- A nonfinancial group is an expanded affiliated group that, for its most recent three-year period, meets all four of the following criteria:

- Has no more than 25 percent of its combined gross income, excluding income of startup companies and entities in liquidation or bankruptcy and income derived from intercompany transactions between members of the expanded affiliated group, consisting of passive income;

- Has no more than 5 percent of its combined gross income, excluding intercompany income, derived from members of the expanded affiliated group that are FFIs

- Has no more than 25 percent of the value of its combined assets held by the expanded affiliated group, excluding assets of startup companies and entities in liquidation or bankruptcy and intercompany assets, that produce or are held for the production of passive income

- Any FFI member of the expanded affiliated group is a participating FFI or deemed-compliant FFI

- This is a significant NFFE category, as many multinational enterprises have one or more foreign entities in their group structure that operates as a holding company, treasury center or captive finance company that might otherwise appear to meet the definition of an FFI on a standalone basis but avoids FFI treatment as a member of a nonfinancial group.

- Startup companies – Entities with no operating history expecting to operate a nonfinancial business

- Entities in liquidation or bankruptcy

- Section 501(c) foreign organizations that have been issued a determination letter from the IRS, as well as other not-for-profit organizations exempt from taxation in their country of residence

Direct Reporting NFFE – An NFFE that elects to directly report information annually about its substantial U.S. owners to the IRS on Form 8966. A direct-reporting NFFE must register on the IRS portal to obtain a GIIN and must disclose its GIIN on Form W-8BEN-E or W-8IMY to qualify for exemption from the FATCA withholding tax, but is not required to enter into an FFI agreement.

- This may be a preferable option if an NFFE otherwise would be a passive NFFE having substantial U.S. owners and the NFFE does not wish to divulge the names, addresses and identifying numbers of its substantial U.S. owners to its U.S. customers on Form W-8BEN-E or W-8IMY due to privacy or other reasons.

Sponsored Direct Reporting NFFE – An NFFE engaging another qualifying entity to act as its sponsoring entity; the sponsoring entity registers the NFFE with the IRS and reports information about the NFFE’s substantial U.S. owners to the IRS on Form 8966.

Passive NFFE – All other NFFEs not falling under any of the NFFE categories listed above

- A passive NFFE must disclose the names, addresses and taxpayer identification numbers of its substantial U.S. owners, if any, on Form W-8BEN-E or W-8IMY in order to qualify for exemption from the FATCA withholding tax

- A “substantial U.S. owner” is any specified U.S. person that owns more than 10 percent (by vote or value) of the passive NFFE; a “specified U.S. person” includes a U.S. citizen, U.S. resident individual and most U.S. entities

- Some types of U.S. entity owners are not treated as specified U.S. persons and thus are not required to be disclosed on Form W-8BEN-E or W-8IMY; these include publicly traded U.S. corporations and their U.S. affiliates, Section 501(c) tax-exempt not-for-profit organizations, IRAs, U.S. federal or state governmental entities, U.S. banks, REITs, U.S. mutual funds and other regulated investment companies, common trust funds and charitable trusts.

Read more at: Tax Times blog