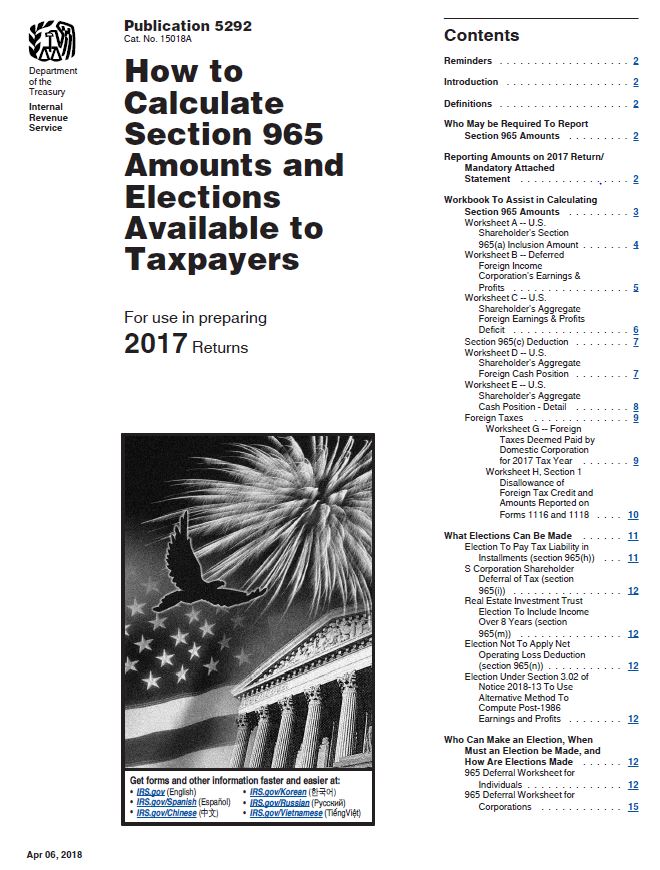

IRS has released Publication 5292 - How to Calculate Section 965 Amounts and Elections Available to Taxpayers. Code Sec. 965, which was amended by the Tax Cuts and Job Act, requires certain foreign corporations to increase their subpart F income for their last tax year that begins before Jan. 1, 2018, by the amount of their deferred foreign income.

The Publication provides a workbook and instructions to assist in calculating "section 965 amounts," and also includes worksheets for taxpayers who may be able to make certain elections with respect to Code Sec. 965.

Publication 5292 includes:

- Worksheet 1.1, the 965 Workbook (Worksheets to Calculate Inclusion of Deferred Foreign Income Upon Transition to Participation Exemption System),

- Worksheet A (U.S. Shareholder's Section 965(a) Inclusion Amount);

- Worksheet B (Deferred Foreign Income Corporation's Earnings & Profits);

- Worksheet C (U.S. Shareholder's Aggregate Foreign Earnings & Profits Deficit);

- Worksheet D (U.S. Shareholder's Aggregate Foreign Cash Position);

- Worksheet E (U.S. Shareholder's Aggregate Cash Position - Detail);

- Worksheet G (Foreign Taxes Deemed Paid by Domestic Corporation for 2017 Tax Year); and

- Worksheet H (Section 1 Disallowance of Foreign Tax Credit and Amounts Reported on Forms 1116 and 1118).

Elections. A U.S. shareholder of a DFIC may elect to pay the Code Sec. 965 net tax liability in eight installments. In addition, owners and beneficiaries of U.S. shareholder pass-through entities may also make elections. Publication 5292 also includes worksheet for taxpayers who may be able to make these elections with respect to Code Sec. 965:

- an election to pay the Code Sec. 965 net tax liability over eight years;

- (ii) an election by S corporation shareholders to defer payment of the Code Sec. 965 net tax liability with respect to such S corporation until a triggering event;

- (iii) an election by real estate investments trusts to take both Code Sec. 965(a) inclusions and the corresponding Code Sec. 965(c) deductions into account over eight years;

- (iv) an election not to apply a net operating loss; and

- (v) an election to use an alternative method to calculate post-'86 earnings and profits (post-'86 E&P).

Publication 5292 provides:

- Worksheet 2.1 and 2.2,

- 965 Deferral Worksheet for Individuals (Calculation of Net 965 Tax Liability to be Paid in Installments); and

- Worksheet 3.1, 965 Deferral Worksheet for Corporations (Corporate Report of Net 965 Tax Liability, Election to Pay Net 965 Tax Liability in Installments Under Subsection 965(h) and Real Estate Investment Trust Deferral of Section 965(a) Inclusion Under Subsection 965(m)).

Marini & Associates, P.A.

Read more at: Tax Times blog

{kind=link}