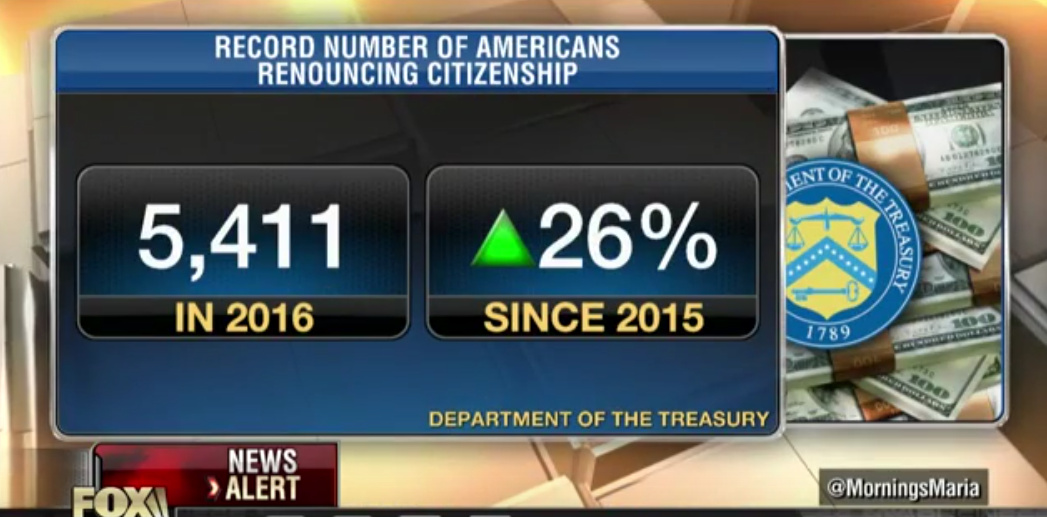

On November 6, 2019 we posted Ten Facts About Tax Expatriation - Part I, where we discussed that whatever your motives, just because you leave the United States and renounce your citizenship, don't assume you can leave U.S. taxes (or U.S. tax forms and complexity) behind, particularly if you are financially well-off.

For those who expatriate after June 16, 2008, the rules are different, since Internal Revenue Code Section 877A applies instead of Section 877. You are subject to an immediate exit tax, which deems you (for tax purposes) to have sold all of your worldwide property for its fair market value the day before your departure from the U.S.

We also discussed in Ten Facts About Tax Expatriation - Part I:

1. Uncle Sam taxes income worldwide.

2. Expatriating means really leaving.

3. The old 10-year window is closed.

4. Big changes came in 1996.

Thirty years later, in 1996, after the Forbes story on "The New Refugees" created a stir, Congress tried again. As part of the Health Insurance Portability and Accountability Act of 1996 (otherwise known as HIPAA), Congress added a presumption of tax avoidance if an expatriate's five-year average net income tax exceeded $100,000, or if the expatriate's net worth was $500,000 or more (both adjusted each year for inflation). But people could--and with the help of skilled lawyers did--rebut the presumption, and the IRS still had to show tax avoidance in most cases.

5. Tax avoidance is now irrelevant.

In 2004 (in the American Jobs Creation Act), Congress threw out the tax avoidance motive test altogether, imposing 10 years of U.S. tax on U.S. source gross income and gains on a net basis if you left the country for any reason. However, Congress increased the threshold for determining who was subject to this expatriation tax. An individual was only subject to the expatriation tax if he had an average net annual income tax for the five years preceding expatriation of $124,000, or if he had a net worth of $2 million or more on the date of expatriation. (If you expatriated on or after June 17, 2008, under the new Section 877A, there is a higher net worth threshold--currently $145,000 of annual net income tax for 2010.)

In some cases, even if you're below these thresholds, you'll get taxed. For example, expatriates must certify their past U.S. tax compliance by filing an IRS Form 8854. Any expatriate who fails to certify compliance with U.S. federal income tax laws for the five taxable years preceding expatriating is subject to the expatriate income tax even if he didn't meet the income tax liability or net worth tests.

Plus, later U.S. visits can be expensive if you expatriated before June 17, 2008 (and Internal Revenue Code Section 877 applies). In that case if an expatriate comes back to the U.S. for more than 30 days in any year during the 10 years following expatriation, that person is considered a resident of the U.S. for that whole tax year. That means the person would again be subject to U.S. tax on his worldwide income, not just his U.S.-source income. Ouch!

This 30-day rule does, however, have an exception for any days (up to a 30-day limit) that the individual performed personal services in the U.S. for an employer (who is not related). This exception only applies if that individual either had certain ties with other countries or was physically present in the U.S. for 30 days or less for each year in the 10-year period on the date of expatriation or termination of residency.

6. There are special rules for long-term residents.

It's easy to define who is or is not a U.S. citizen, but the term "long-term resident" isn't quite so clear. A long-term resident is a non-U.S. citizen who is a lawful permanent resident of the U.S. in at least eight years during the 15-year period before that person's residency ends. A "lawful permanent resident" means a green card holder. However, a person is not treated as a lawful permanent resident for purposes of this eight-year test in a year in which that person is treated as a resident of a foreign country under a tax treaty, and does not waive the treaty benefits applicable to the residents of that country. Caution: holding a green card for even one day during a year will taint the whole year.

7. There's an exit tax for expatriations on or after June 17, 2008.

The Heroes Earnings Assistance and Relief Tax Act of 2008 (generally known as the Heroes Act) changed the method of taxation for those who became expatriates on or after June 17, 2008, adding even more complexity and usually higher U.S. taxes. If you are a U.S. citizen or long-term resident who expatriates on or after June 17, 2008, you will be deemed (for tax purposes) to have sold all of your worldwide property for its fair market value the day before you leave the U.S.! All that gain is subject to U.S. tax at the capital gains rate. Plus, all your gain is taken into account without regard to any ameliorative tax provisions in the Internal Revenue Code.

Put differently, you get all of the bad parts of the tax code, and none of the good. That would include, for example, the inability to benefit from the $250,000 per person ($500,000 per couple) exclusion from gain on a principal residence (Section 121 of the Internal Revenue Code) and many other rules. The exit tax is like an estate tax, in the sense that everything that would be part of your estate will be subject to income tax on unrealized gains as of the day before you expatriate, as if you sold all your assets the day before leaving. In effect this is Congress' way of making sure your assets don't escape the estate tax entirely through expatriation.

Marini & Associates, P.A.

Read more at: Tax Times blog